Continents

Countries

Clients

Colleagues

Users

The digital race is on.

Are you in it to win it?

If you’re beset by slow time-to-market, costly development projects, legacy constraints and vendor lock-in, the answer is probably no. Here’s how we can help you get ahead of the game.

Drive innovation with fully-fledged digital banking solutions

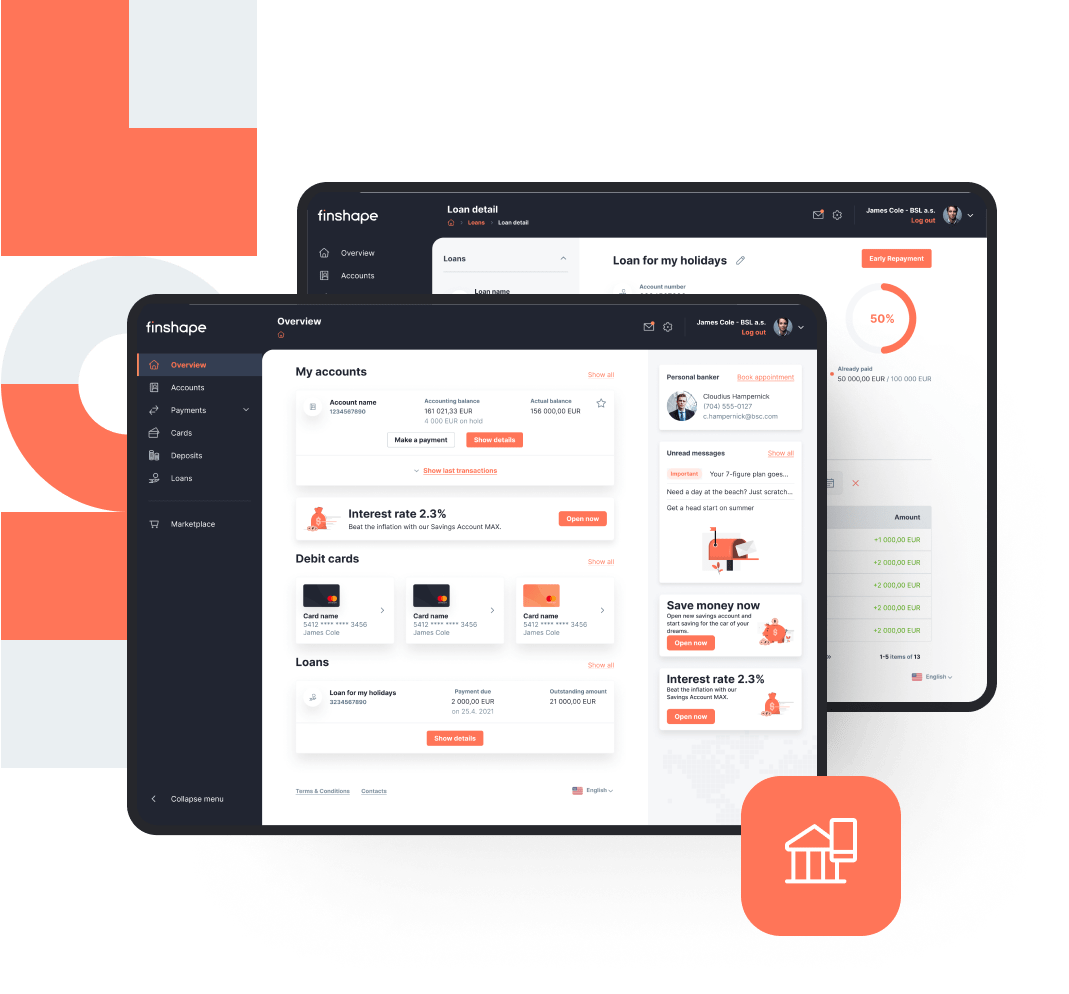

Digital banking

Make daily banking a breeze and turn customers, retail, business or wealth management, into brand advocates, while boosting revenues and cutting costs.

Digital sales

Find new ways to identify and address customer needs and maximise revenue at every touchpoint across the customer lifecycle.

Client acquisition

Address prospect customers in digital space with onboarding process that is faster, easier and as safe as, if not safer than, in-branch banking.

Personalised targeting

Find the perfect moments to reach out to customers, design interactions that matter and convert channel traffic to sales.

New product sales

Make it easier for customers to apply for banking products through streamlined processes with minimal effort and data input required.

Customer engagement

Turn your customers into powerful brand advocates by consistently exceeding their expectations.

Customer journeys

Deliver the right experience through the right channel based on your customers’ needs, habits and preferences.

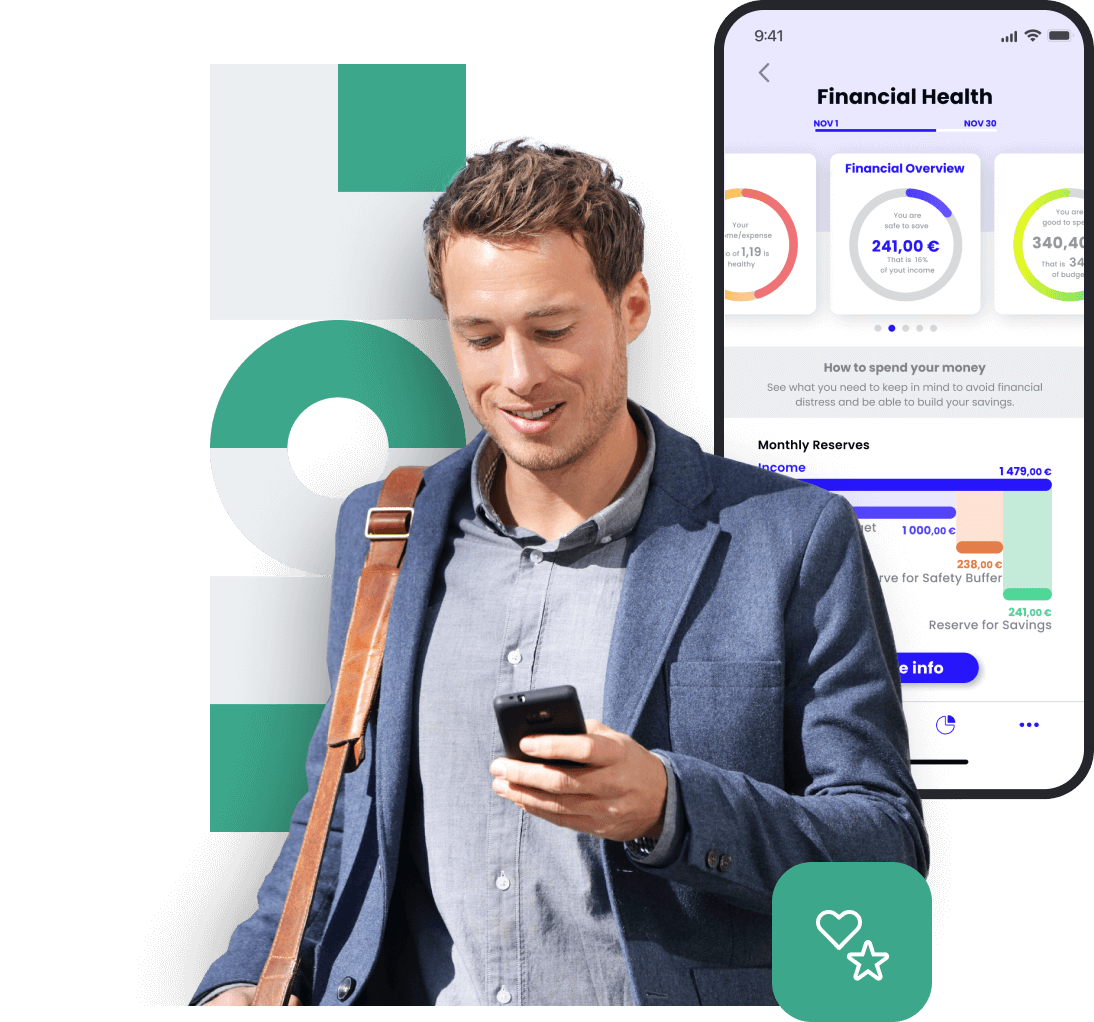

Personalised Financial Insights

Send bite-sized alerts, summaries and reminders to help customers make better financial decisions, big or small.

Composable banking

Customer portal

Enable your customers to easily access any information or resource they need online and on-the-go, including notifications, documents, products and services.

Extended banking

Boost your product and service offering by integrating it with other financial or non-financial service providers- and let customers reap the benefits

Discover ready-made digital products

Reduce costs, risk and time-to-market and build next-generation digital capabilities with our tried and tested, ready-to-use digital products.

Chat with us

Schedule an appointment with one of our colleagues so we can discuss your specific needs. Fill in the form and we’ll get back to you in no time.