Over the past couple of months, we’ve shared our two cents on why personalisation matters, what keeps banks from embracing it, and how they can get it right and turn it into a win-win. Now let’s get down to the nitty-gritty. Here are the five stages of setting up a banking personalisation platform like a pro and making the most of it, as seen by Gellért Vinnai, W.UP’s head of product.

Step 1: Beef up your data

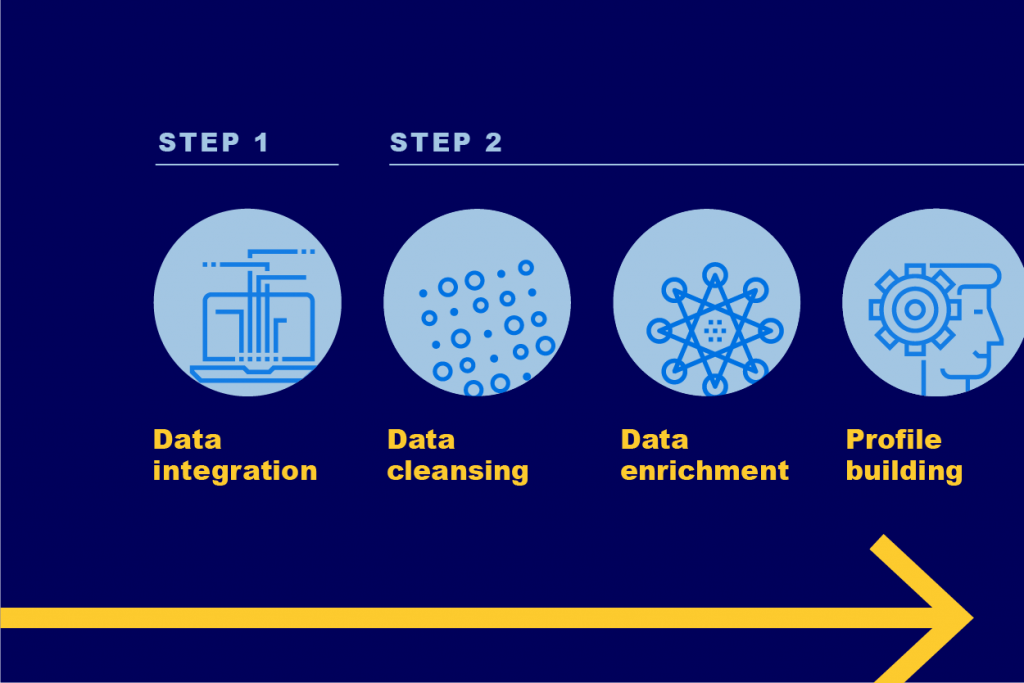

Personalisation starts with finding out who your customers are, what they like (and what they don’t) and how they live their lives based on data. So the first step is to gather as much information about them as possible, from as many data sources as possible, and integrate it into a single platform. Of course, that’s easier said than done. Long-standing financial institutions tend to have a mixed bag of IT infrastructure, with systems, older and newer, layered upon each other over the decades.

Meaning that banking customer data is often scattered across an account management system, a CRM, a card management system and more.

Data integration helps banks merge all this data together and also blend in other, less traditional data sources. Think geolocation data collected through mobile phones or information on how and how often people use various banking channels. Plus, in our brave new post-PSD2 world, banks can also find out what other financial service providers their customers use and what for.

Sounds dreamy, doesn’t it? But there’s a catch. Well, sort of. “Banks must stay mindful of underlying privacy concerns. No matter who collects it or where, the owner of customer data is the customer. This is why it’s extremely important for banks to be transparent about what they do with it, ask customers for consent directly and tell them how they will benefit from sharing their data,” Gellért explains.

Step 2: See customers for who they really are

Once you have enough data, it’s time to make it work for you. First, take care of data hygiene and give your datasets a thorough cleansing to make sure that all records are complete, correct, accurate and relevant. Then comes data enrichment, aka refining raw data to the point that it actually makes (business) sense. In the case of transactions, for instance, data enhancement means that they can be categorised by type or frequency or marked as regular or outlier transactions. “Results of such analyses vary greatly. A transaction can be nothing special for one customer and once in a lifetime for another,” Gellért says.

Now that you have all your data prepped, you can start building customer profiles to get a better picture of what your customers are like on an individual level. Do they have a car or use public transportation? Are they into fine dining or fast food? Where and how often do they do their grocery shopping? This is carried out with the help of machine learning clustering algorithms. Gellért points out: “What we do is set up certain search criteria based on which algorithms identify relevant groups of customers. Then we take these clusters and translate them into business insights and a fixed set of rules.”

He continues: “One of the biggest benefits of our platform is that banks don’t need to build any of this from scratch. All they need to do is figure out how our pre-built profiles can be used and configured in a way that suits their business, sales and marketing strategies best.”

And that’s just scratching the surface. Stay locked on our blog for part two of this post and learn how to target the right customers with the right offer at the right time as well as how personalisation can help you achieve your business goals while making (and keeping) customers happy.