It’s science, people.

In 1999, MIT professors-slash-economists Drazen Prelec and Duncan Simester held a silent auction for five hundred students on the MIT campus. The unsuspecting participants had the opportunity to get their hands on tickets to sold-out Celtics basketball games. Half of them, however, were told they could only pay with cash, while the researchers told the other half they could only pay with their credit card. What happened next was not something the economist duo had seen coming.

“On average, we found that the credit card buyers bid more than twice as much as the cash buyers bid,” Professor Prelec summed up their findings. “That’s got to be crazy, right? It suggests that the psychological cost of spending a dollar on a credit card is only fifty cents.” The reason behind this, however, makes perfect sense. Credit cards, as the researchers concluded, disconnect the act of buying something, which brings people joy, from the act of paying for it, which causes them pain.

“The moral tax gets blurred with credit cards. When you’re consuming, you’re not thinking about the payments, and when you’re paying, you don’t know what you’re paying for,” the economist explained. As a result, people dread credit card bills more than they do parking tickets. In fact, one of the reasons more and more banking customers reach for their debit cards instead is to avoid credit card fears. “There’s no good reason to prefer debit cards over credit cards, unless we have learned to dread the credit card bill.”

There’s no good reason to prefer debit cards over credit cards, unless we have learned to dread the credit card bill.Drazen Prelec, Professor, MIT

So how can banks help people build better relationships with money and, in broader terms, with banks themselves?

Everyone knows it’s important to keep an eye on their spending but not many of us actually do so. That said, not many of us have access to key spending insights, especially in a way that makes sense. Science seems to back this idea up. “What’s important is feedback,” psychologist and behavioural economist Emir Efendic is quoted to explain in a BBC Future article. “With credit cards, you don’t get instant updates. But with online banks, you see the amount deducted immediately,” Efendic argues.

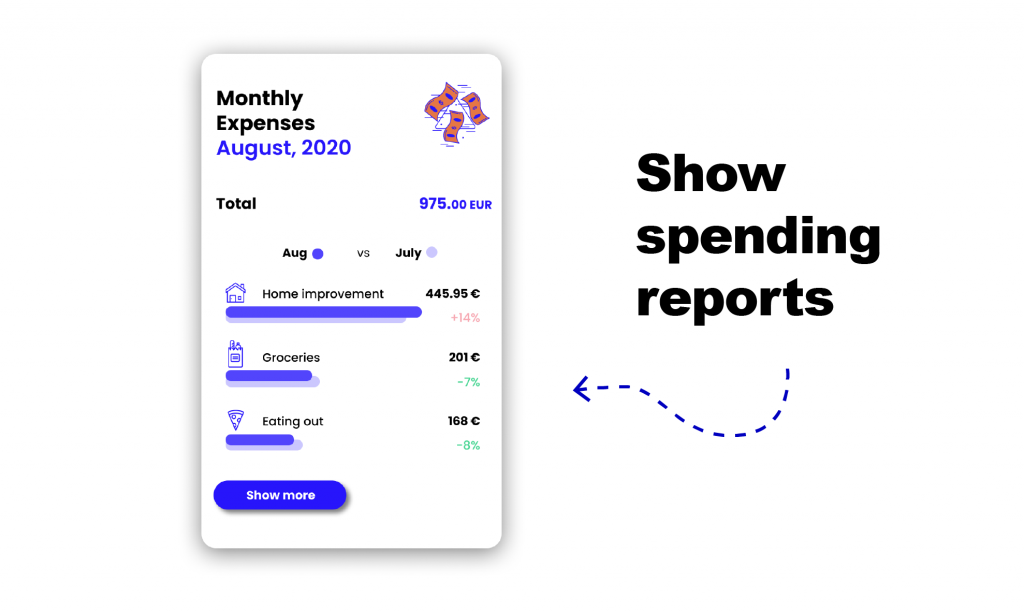

Spending Report from the W.UP Personalisation Platform

In other words, real-time, easy-to-grasp information on what customers do with their money can have a transformative effect on how they view finances, financial products and financial service providers. Using nothing else than current account and transactional data, banks can break down spending by date, merchant or category and show customers how much money they need for necessities like food, utility bills and loan repayments and how much they can splurge on non-essential items, such as restaurant dinners or movie tickets. Not to mention holidays. It’s not easy to gauge the total expense of a trip based on monthly reports. A detailed travel spending summary, however, can give customers a much better idea of how much to earmark for their upcoming trip.

And that’s not all. Not only do spending insights empower banking customers to spend less or better, but they’re also a great way to encourage digital interactions. The more people use and trust digital banking channels, the more opportunities there are for banks to learn more about their behaviour, boost engagement and build loyalty.